Filters

Question type

Exhibit 9-16  Exhibit 9-16 depicts the cost and demand conditions facing a profit-maximizing monopolist that does not price discriminate.Which of the following statements is true?

Exhibit 9-16 depicts the cost and demand conditions facing a profit-maximizing monopolist that does not price discriminate.Which of the following statements is true?

A) An output of 50 is allocatively efficient, but the monopolist will produce 100 units.

B) An output of 50 is allocatively efficient, but the monopolist will produce 75 units.

C) An output of 75 is allocatively efficient, but the monopolist will produce 100 units.

D) An output of 100 is allocatively efficient, but the monopolist will produce 50 units.

E) An output of 100 is allocatively efficient, but the monopolist will produce 75 units.

F) C) and D)

G) All of the above

G) All of the above

Correct Answer

verified

Correct Answer

verified

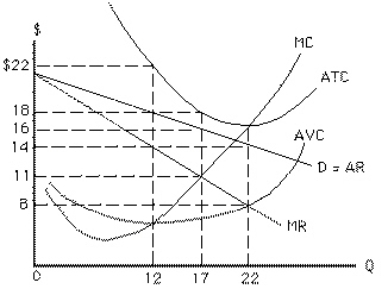

Exhibit 9-14  At the profit-maximizing (or loss-minimizing) level of production, the monopoly in Exhibit 9-14 will have total cost of

At the profit-maximizing (or loss-minimizing) level of production, the monopoly in Exhibit 9-14 will have total cost of

A) $264

B) $306

C) $216

D) $187

E) $176

F) A) and E)

G) B) and E)

G) B) and E)

Correct Answer

verified

Correct Answer

verified